Features

Management

Navigating the cannabis insurance marketplace

What Canadian cannabis companies should consider when obtaining insurance

April 12, 2022 By Kyle Muscat

Many insurers still view cannabis as a higher risk class, while the lack of established historical losses add a factor of ambiguity into their pricing decisions. Photo: TimeStopper/Adobe stock

Many insurers still view cannabis as a higher risk class, while the lack of established historical losses add a factor of ambiguity into their pricing decisions. Photo: TimeStopper/Adobe stock The insurance requirements imposed upon cannabis producers add yet another layer of complexity to an industry already defined by onerous regulatory challenges and red tape. From banks and alternative capital providers, business partners, provincial wholesalers and board members; management must answer to a variety of stakeholders – each with their own unique insurance demands.

Having been more than three years since the legalization of recreational use (and significantly longer on the medical side), the Canadian cannabis insurance marketplace can be still be viewed to remain in its infancy stage; defined by a lack of market participants and competitive product offerings. For producers, this means a limited number of insurers to choose from, more restrictive terms and greater annual premiums than those levied against organizations operating within comparable industries.

There is generally limited interest on behalf of insurers to compete in the sector. This is largely due to management’s priorities and the resources required to develop internal underwriting expertise while capturing enough written premium to make the venture worthwhile. This would demand a shift in focus away from larger, more traditional industry classes for which they are still trying to grow.

Similarly, insurers still view cannabis as a higher risk class while the lack of established historical losses add a factor of ambiguity into their pricing decisions. Additional consideration can be given to Canadian insurers with U.S. domiciled head offices (where cannabis remains federally illegal) and compliance with their reinsurance partners who may exclude or have limited appetite for this class of risk.

Industry pain points

Directors and officers

Generally speaking, Directors and Officers (D&O) insurance protects an organization’s individual executives, directors, and officers from personal financial loss that may result from allegations of wrongful acts or mismanagement carried out in their appointed capacity. Purchased by both publicly-traded and private organizations alike, this coverage is often a necessary safety net required to attract experienced board members and management.

Although we have observed notable development in the D&O market over the past few years, cannabis-related businesses remain at the mercy of a relatively limited number of carriers. Coverage is frequently offered with restrictive covenants and remains challenged for organizations holding U.S. assets. Many licensed producers are forced to obtain policies from specialty markets or unlicensed carriers domiciled in foreign jurisdictions.

Product recall

As the name suggests, Product Recall insurance is designed to protect against the financial impacts associated with both voluntary and government-mandated product recalls. In addition to the actual value of recalled goods, this extends to include the cost of notifying customers and supply chain participants along with withdrawal, shipping, and disposal expenses.

These policies often include coverage for extra expenses incurred to minimize the suspension of business operations with dedicated limits for public relations and reputational brand protection.

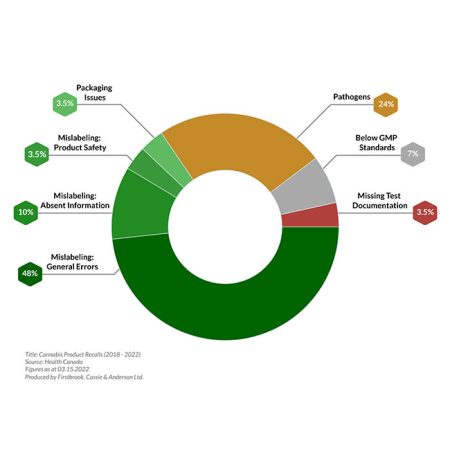

At the time of writing, there have been more than 132,000 units of recalled cannabis products in Canada – largely emanating from mislabeling and packaging errors.

It’s important to note that this form of insurance is a prerequisite requirement when supplying products to select provincial wholesalers. For example, the Ontario Cannabis Store (OCS) mandates licensed producers to carry $15 million of recall coverage, whereas the BC Liquor Distribution Branch (BCLDB) in British Columbia requires a minimum of $10 million – with few exceptions.

Crop spoilage

Although widely available across the broader Canadian agricultural industry, crop spoilage is another form of coverage which remains challenged for cannabis producers. This covers live plants and biological assets; protecting organizations against the financial impacts of plant disease, infestation, or other forms of loss during the growing phase. Coverage is also available for the loss of perishable product as a result of a power outage and machinery breakdown.

This form of insurance often remains prohibitively expensive for most organizations, although we do expect to see further market participants enter the space in the coming years.

Cannabis Product Recalls (2018 – 2022)Photo: firstbrook, cassie & anderson ltd.

Insurance blind spots

Excise duty security bonds

Cannabis producers are all too familiar with the security requirements imposed upon them under the Excise Act. Simply put, the cannabis excise duty regime requires all registered participants to provide the Canadian Revenue Agency (CRA) with security in an amount that ranges anywhere from $5,000 to $5 million. This is most often in the form of cash or an irrevocable letter of credit (LOC). While an LOC is most commonly used, the value of which must still be securitized against an operational line of credit or cash in the bank – effectively limiting the amount of working capital that would otherwise be available to fund operations.

An excise duty surety bond is a financial instrument that functions very similar to a LOC, however it is underwritten and issued on behalf of an insurance company in consideration for an annual premium. In this context, a bond could be viewed as an unsecured ‘secondary’ line, supported by the insurance markets.

As an acceptable form of security to the CRA, cannabis producers are increasingly utilizing L302 cannabis excise bonds to free up working capital while maintaining regulatory compliance. With an annual premium levied at a rate of one to three per cent of the bond amount, producers are quick to realize the benefits of this product when compared against their own internal rate of return.

Transactional insurance products

Consolidation has been an undisputed hallmark of the cannabis industry. While relatively underutilized, transactional insurance products can be leveraged to insulate organizations against the financial risks involved in the purchase, sale, or merger of companies. This is more commonly known as Reps & Warranties, Tax and Contingent liability insurance. The financial clarity afforded under these policies often benefit both sides of the transaction through a reduction in indemnity escrow requirements, more attractive terms and increased deal expediency. One caveat here would be that a deal size threshold of $25 million is often required before these polices start to make sense.

Cyber Insurance

Most industry experts would agree that cyber security is no longer a hypothetical risk for Canadian businesses. Cyber criminals continue to develop increasingly complex methods of exploitation while making headlines across nearly every industry. Meanwhile, the pandemic has further accelerated the digitization of most organizations.

In addition to proactive cyber security protocols, cannabis producers can purchase insurance to further protect themselves from this risk. These policies extend to include coverage for data remediation, cyber extortion, and financial loss due to a suspension in operations. There are also dedicated limits for reputational repair along with regulatory investigations and fines that may be imposed for breaching PIPEDA or PHIPA – the Canadian personal and health information protection acts. It is increasingly evident that the severity of this emerging risk cannot be understated.

Looking forward

It is fair to say that the wider insurance industry has been slow to respond to the complex risks faced by cannabis producers. Now more than ever, it is imperative that producers partner with an experienced broker who can effectively navigate the rapidly evolving insurance landscape.

Kyle Muscat leads the cannabis insurance practice at Firstbrook, Cassie and Anderson Ltd. – a leading Canadian insurance brokerage and risk management firm. Operating under the CannaCover trade name, their practice offers bespoke insurance solutions for licensed producers and the broader Canadian cannabis industry.

Print this page